Your business’s financial statements give you a snapshot of the financial health of your company. Without them, you wouldn’t be able to monitor your revenue, project your future finances, or keep your business on track for success.

Now, you can’t go off creating your different financial statements all willy nilly. Like many things in business, you have to follow an order.

Read on to learn the order of financial statements and which financial statement is prepared first.

Overview of financial statements

Before you can dive into the order of financial statements, find out what the main financial statements are. Check out a quick overview below of the four types of financial statements in accounting.

Cash flow statement

Your cash flow statement, or statement of cash flows, is all of your business’s incoming and outgoing cash. Basically, your cash flow statement shows you how much cash flows in and out of your business. Your statement of cash flows only records the actual cash your company has.

There are three parts of a cash flow statement: operations, investments, and finances.

Your cash flow might be positive, meaning that your business has more money coming in than going out. Or, your company could be in negative cash flow territory, which indicates that you’re spending more money than what you’re bringing in.

Investors, lenders, and vendors might be interested in checking out your business’s cash flow statement. That way, they can see whether or not your company is a good investment.

You can even use your cash flow statements to create a cash flow forecast or projection. A cash flow projection lets you estimate the money you expect to flow in and out of your business in the future. Forecasting your business’s future cash flow can help you predict financial problems and give you a clear picture of your company’s financial future.

Balance sheet

Your balance sheet tracks your financial progress over time and has three different parts that you may already be familiar with:

- Assets

- Liabilities

- Equity

Your assets are items of value and things that your business owns. A few examples of assets include company vehicles and inventory. Your assets can be current or noncurrent. Current assets are items of value that can convert into cash within one year (e.g., checking account). Noncurrent assets are items of value that take more than one year to convert into cash.

Liabilities are debts you owe to other individuals, such as businesses, organizations, or agencies. Your liabilities can either be current (short-term) or noncurrent (long-term). Some examples of liabilities include accounts payable, accrued expenses, and long-term loan debt.

Equity is everything you own minus your liabilities and debts. You can easily find equity by using the following formula:

Equity = Assets – Liabilities

Your total assets should equal your total liabilities and equity. If they don’t, your balance sheet is unbalanced, and you need to find what’s causing the discrepancy between your assets, liabilities, and equity.

Your balance sheet is a big indicator of your company’s current and future financial health. Use your balance sheet to find out where you stand financially. You can also use your balance sheet to help you make guided financial decisions.

Income statement

Your income statement, also called a profit and loss statement (P&L), reports your business’s profits and losses over a specific period of time. You can use an income statement to summarize business operations for a certain time frame (e.g., monthly, quarterly, etc.).

Your income statement begins with sales and ends with net income or loss. Some other parts you might see on your income statement include:

- Revenue

- Cost of goods sold

- Expenses

- Taxes

- Gross profit

- Depreciation

- EBIT/EBITDA

- Other financial gains and costs

Your income statement gives you insight into your company’s income and expenses. Use your income statement to see how profitable your business is. The last line of your income statement, called the bottom line, shows you net income or loss.

If you want to assess your business’s profitability over a specific time period, check out your income statement.

Statement of retained earnings

Your statement of retained earnings, or statement of owner’s equity, lists what your business’s retained earnings are at the end of an accounting period. Retained earnings are profits you can use to pay off liabilities or make investments.

You can use your statement of retained earnings independently. Or, you can add your retained earnings statement to your balance sheet.

If your statement of retained earnings is positive, you have extra money to pay off debts or purchase additional assets.

To create a statement of retained earnings, you need the retained earnings formula. Take a look at the retained earnings formula below:

Retained Earnings = Beginning Retained Earnings + Net Income – Dividends Paid

Use the formula above to help calculate your retained earnings balance at the end of each period.

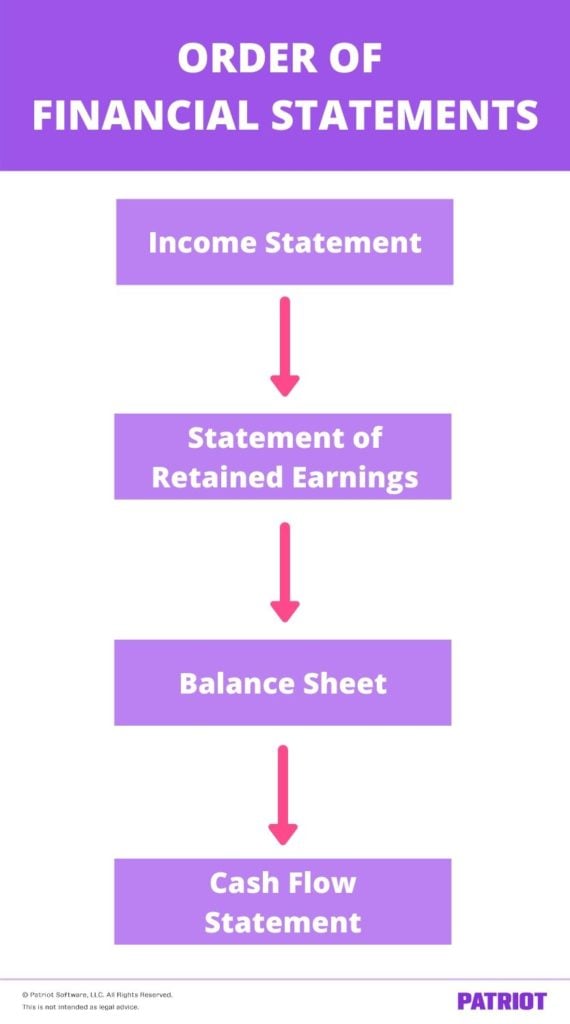

Which financial statement is prepared first?

Now that you know all about the four basic financial statements, read on to learn what financial statement is prepared first.

1. Income statement

The financial statement prepared first is your income statement. As you know by now, the income statement breaks down all of your company’s revenues and expenses. You need your income statement first because it gives you the necessary information to generate other financial statements.

Revenues would be any sales that your business generates. Expenses could be various operating costs, like inventory, rent, or utilities.

Generate your income statement first so you can see your business’s net income and analyze your sales vs. debt.

When creating your income statement, list revenues first. Then, list out any expenses your company had during the period and subtract the expenses from your revenue. The bottom of your income statement will tell you whether you have a net income or loss for the period.

2. Statement of retained earnings

Your statement of retained earnings is the second financial statement you prepare in your accounting cycle.

Use your net profit (or net loss) from your income statement to prepare your statement of retained earnings. After you gather information about your net profit or loss, you can see your total retained earnings and how much you’ll pay out to investors (if applicable).

3. Balance sheet

After you generate your income statement and statement of retained earnings, it’s time to create your business balance sheet. Again, your balance sheet lists all of your assets, liabilities, and equity. Your total assets must equal your total liabilities and equity on your balance sheet.

Use the information from your income statement and retained earnings statement to help create your balance sheet.

Create your balance sheet and include any current and long-term assets, current and noncurrent liabilities, and the difference between your assets and liabilities (aka equity).

4. Cash flow statement

Last but not least, use all of your financial data from your other three statements to create your cash flow statement. Your cash flow statement shows you how cash has changed in your revenue, expense, asset, liability, and equity accounts during the accounting period.

Prepare your cash flow statement last because it takes information from all of your other financial statements.

After you generate your final financial statement, use your statements to track your business’s financial health and make smart financial decisions.

Looking to streamline your accounting process? Patriot’s accounting software lets you keep your expenses and income organized and up-to-date so that your financial statements don’t suffer. Start your free trial today!

This is not intended as legal advice; for more information, please click here.