When it comes to your small business, there are a number of financing options available. A couple of popular options include a business loan or credit card. But, which one is better for your business? Get to know the difference between business loan vs. credit card and learn how to decide between the two.

What’s the difference between a business loan vs. credit card?

Understand business loan vs. business credit card starting with the basics: definitions.

What is a business loan?

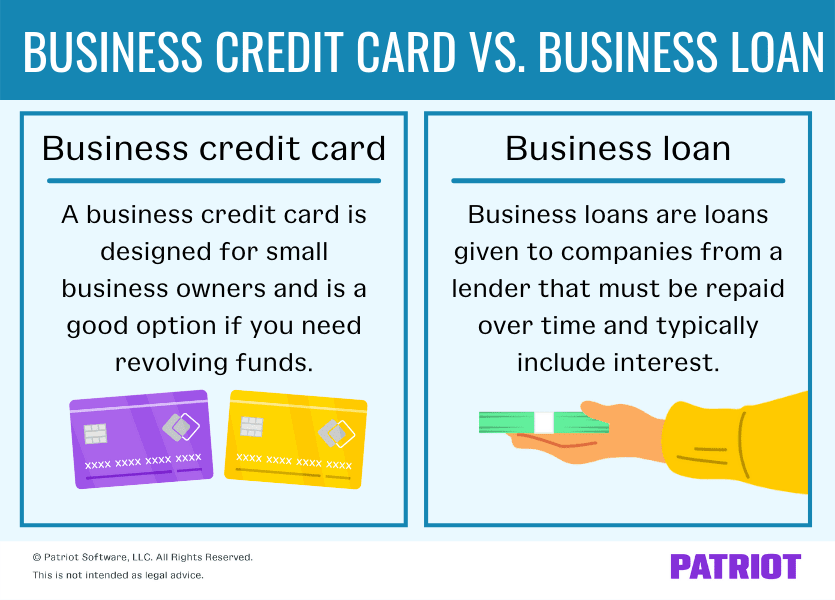

Business loans are loans given to companies from a lender (e.g., bank) that must be repaid over time and generally include interest.

A business loan can come in many different shapes and sizes. There are a ton of different loan types out there for business owners to choose from. Here are a few you may consider looking into:

- Bank loan

- SBA loan

- Term loan

- Short-term loans

- Long-term loans

- Microloans

- Disaster loans

Certain types of loans are better for different situations. For example, disaster loans are specifically for businesses struggling due to declared disasters (e.g., natural disasters).

With many loans, you’ll receive the funds upfront and pay back the money you owe in installments. However, each type of loan works differently and may have different rules.

Applying for a business loan can be an easy process if you prepare ahead of time and meet the credentials. Generally, you need to:

- Determine how much you need

- Choose a loan

- Review your credit score and history

- Gather documents (e.g., financial statements)

- Fill out an application (in person or online, depending on the lender)

What is a business credit card?

Just like how you can get credit cards for personal use, you can also get credit cards specifically for business use. A business credit card is designed for small business owners and is a good option if you need revolving funds.

Business credit cards work similarly to personal or consumer credit cards, but generally offer certain perks just for businesses. By getting a business credit card, you can:

- Build up credit

- Access rewards (e.g., cashback on business purchases)

- Simplify cash flow

- Protect your business financially

Like with a business loan, you need to go through an application process to get a business credit card. Before you try to get a business credit card, you should review your credit and research card options. Once you have a good idea of what card is best for your business you can apply by:

- Gathering information (e.g., personal and business information)

- Processing the application (generally online)

- Waiting to hear back from the card issuer

In most cases, getting a business credit card is a quick and painless process as long as you do your research, gather the necessary information, and are qualified. And, you can typically just apply online and hear back within a few business days.

What’re the pros and cons of business credit cards and loans?

Of course, there are pros and cons to everything in business. Before you decide to go a certain route financing-wise, take a look at the advantages and disadvantages of both business credit cards and business loans.

Business loans

Here are a few advantages and disadvantages of getting a small business loan for your company.

Pros:

- Can receive large loan amounts, depending on the loan

- May be able to receive all of the money upfront

- Interest rates can be lower than other options (can vary based on your business’s credit and finances)

- Interest payments can be deductible on your taxes

- Helps overcome cash flow challenges

- Can accelerate your business’s growth

Cons:

- Need to apply for new loans if you need additional funding

- Creditors may ask for a personal guarantee and collateral

- May be more funds than you need

- Repayments can damage your cash flow

Business credit cards

Check out a few pros and cons of business credit cards.

Pros:

- Revolving line of credit you can use over and over again

- No collateral needed

- No interest if you pay your balance in full each month

- May offer additional perks, like cashback or discounts

- Can be easy to qualify

- Helps you build credit

- Easy way to finance your small business

Cons:

- Interest rates are typically high

- Fees may apply (e.g., per transaction, annual, or late fees)

- Credit limit could be low

- Most require a personal guarantee (need to show previous personal credit history to qualify)

- May not offer purchase protection like personal credit cards do

Is it better to get a business loan or credit card?

So, are loans or credit cards better for your business? Well, the answer depends on your company’s financial situation and what exactly you’re looking for funding-wise.

Small business loans are a good option if you:

- Need a larger sum of money

- Want to make a large investment or purchase

- Need to refinance existing debt

- Want lower interest rates

Business credit cards are an ideal option if you:

- Need short-term financing

- Want to separate personal and business funds

- Need funds quickly

- Want additional perks, like cashback on purchases, for your business

- Plan on financing ongoing expenses

Again, review the pros and cons of each option before choosing between business credit card vs. loan. Learn what you’re getting yourself into with each option to make a smart selection.

Other financing options to consider…

As a business owner, you aren’t limited to just business loans and credit cards for financing. There are plenty of other ways to fund your business, such as:

- Crowdfunding

- Angel investors

- Venture capitalists

- Small business grants

- Funds from family and friends

- Personal funds

Before you choose to apply for a business loan or credit card or pursue one of the funding options above, do your research. That way, you can determine ahead of time which financing option is the best fit for your business.

This is not intended as legal advice; for more information, please click here.