For 40% of small business owners, handling bookkeeping and taxes is the worst part of owning a business. Sound familiar? If so, you might consider shirking your recordkeeping responsibilities. It’s not a big deal, right? Wrong! Recordkeeping is one of the most important things you can do. And to make things easier on yourself, there are simple recordkeeping for small business tips and tricks you can learn.

Dive into why recordkeeping is so important for your business and how you can streamline the process.

The importance of recordkeeping for small business

Recordkeeping for small business impacts everything from your ability to make financial decisions to filing taxes. In short: recordkeeping is pretty important.

The IRS goes into detail about how keeping good records helps you:

- Monitor your business’s progress

- Prepare financial statements

- Identify sources of income

- Keep track of deductible expenses

- Keep track of your investment in property

- Prepare tax returns

- Support items reported on your tax returns

Monitor your business’s progress

Is your business improving? Staying the same? Which items are selling, and which are growing dust on the shelf?

Recordkeeping lets you find the answers to these questions—and more. You have the information you need to monitor how your business is doing and make more-informed business decisions.

For example, you can use your records to scrap certain products, decide on new pricing strategies, and make marketing decisions.

Prepare financial statements

A financial statement is a collection of your company’s financial information during a period (e.g., month, quarter). You need your business records to prepare financial statements.

There are three main financial statements you can create and analyze:

- Income statement: Your business’s profits and losses

- Balance sheet: Your business’s assets, liabilities, and equity

- Cash flow statement: Your business’s incoming and outgoing money

With accurate records, you can create accurate financial statements. Business owners and their accountants analyze financial statements to determine things like liquidity, profitability, and cash management success.

Not to mention, you need accurate financial statements when applying for business financing (e.g., loans, investments, etc.).

Identify sources of income

Do you receive money or property from more than one source? More than likely, the answer is yes. And if it is yes, you need your records’ help in identifying those sources of income.

That way, you can separate business and non-business receipts. And you can easily separate taxable and non-taxable income, making tax time a little easier.

Keep track of deductible expenses

When you run a business, your tax liability adds up. Luckily, there are deductions you can take to lower your tax bill. But if you want to take advantage of tax deductions, you need detailed and accurate records.

Use your records to keep track of deductible expenses you can claim when filing your small business tax return.

Keep track of your investment in property

Do you invest in property? If so, you want to track your basis, which is the amount of your property investment for tax purposes.

Through clear records, you can calculate your:

- Gain or loss on the sale, exchange, or other property disposition

- Deductions for depreciation, amortization, depletion, and casualty losses

Prepare tax returns

For many individuals and business owners alike, tax time is stressful. Keeping up-to-date records can help ease some of your tax-time stress.

Instead of scrambling at the last minute, keep organized records to support income, expenses, and tax deduction or credit claims.

Consider getting information together ahead of tax time easier. For example, you may gather records like financial statements, invoices and receipts, payroll records, etc.

Support items reported on your tax returns

The last thing any business owner wants is an IRS audit. But, it can happen. And if you get audited by the IRS, you must provide your business records.

Keep clear records—such as receipts, bills, canceled checks, and employment documents—to back up your claims and speed up the IRS audit process.

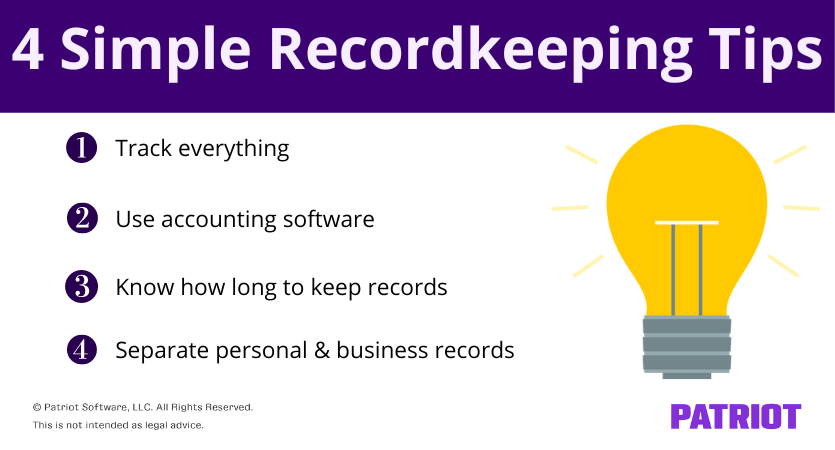

4 Simple recordkeeping for small business tips

So, recordkeeping for small business is important. But how can you manage your recordkeeping responsibilities and keep your sanity?

Check out the following simple recordkeeping for small business tips:

- Track everything—everything!

- Use accounting software

- Know how long to keep records

- Separate your personal and business records

1. Track everything—everything!

Think a receipt is too small to keep? Think again. You should track everything related to business income and expenses.

According to the IRS, it’s best to record transactions daily for accurate recordkeeping. Record business transactions in a:

- Journal (a book where you record business transactions shown on supporting documents)

- Ledger (a book that contains the totals from all your journals, organized by account)

For simple recordkeeping, consider keeping an electronic journal and ledger (e.g., through accounting software).

In addition to tracking transactions in your journal and ledger, keep supporting documents such as:

- Cash receipts

- Bank statements

- Financial statements

- Credit card statements

- Invoices

If you’re an employer, you’ll have a number of additional records to keep, including:

- Withholding forms

- Payroll taxes

- Benefits and deductions

- Time and attendance records

2. Use accounting software

Accounting software isn’t the only method you can use to account for transactions. You can also record transactions by hand using spreadsheets. But when it comes to simple recordkeeping for small business, accounting software can make a big difference.

Some accounting software systems let you do the following in your account:

- Track your expenses, income, and money

- Easily record payments

- Keep records all in one place

- Reconcile your accounts

- Manage receipts and documents

If your accounting software lets you securely upload receipts and other documents, you can attach files to the transactions themselves. And with digital records, you can say goodbye to paper records and disorganization.

3. Know how long to keep records

A key part of recordkeeping is knowing how long to keep records that support your tax return information.

According to the IRS, the length of time depends on the situation:

| Length of Time | Situation |

|---|---|

| 3 years from the date you filed your original return or 2 years from the date you paid the tax (whichever is later) | If you file a claim for credit or refund after filing your return. |

| 6 years | If you do not report income that you should report (and it’s more than 25% of the gross income on your return) |

| 7 years | If you file a claim for a loss from worthless securities or bad debt deduction |

| Indefinitely | If you do not file a return. If you file a fraudulent return. |

If you’re an employer, you also have employment tax records. Keep employment tax records for four years after the date that the tax becomes due or is paid (whichever is later).

4. Separate your personal and business funds

“OK, that receipt was for the new office printer … or was it for my personal printer?”

Regardless of your business structure and size, combining your personal and business funds can get messy. And messy records can slow down your recordkeeping process.

In fact, the IRS recommends keeping separate business and personal accounts for easier recordkeeping.

Separating your personal and business funds can:

- Organize your accounting records

- Make it easier to file your business tax return

- Help you avoid overspending

- Create a clear audit trail

To separate your business records from personal ones, open a business bank account. To get started, you’ll need information like your Social Security number, Employer Identification Number (EIN), and business license.