Creating an employee benefits package can help attract and retain talent. But providing health insurance benefits to your employees can leave you with questions. If employees contribute to their premiums, you have to know how to deduct the cost from their gross pay. Is health insurance pre-tax on payroll?

Read on to learn the answer to this question so you can accurately handle payroll.

Skip Ahead

Is health insurance pre-tax on payroll?

The answer to Are payroll deductions for health insurance pre-tax? is: it depends on the type of health insurance plan you have. Generally, health insurance plans that an employer deducts from an employee’s gross pay are pre-tax plans. But, that’s not always the case.

While shopping for employee health benefits, you may consider either pre-tax or post-tax health insurance options.

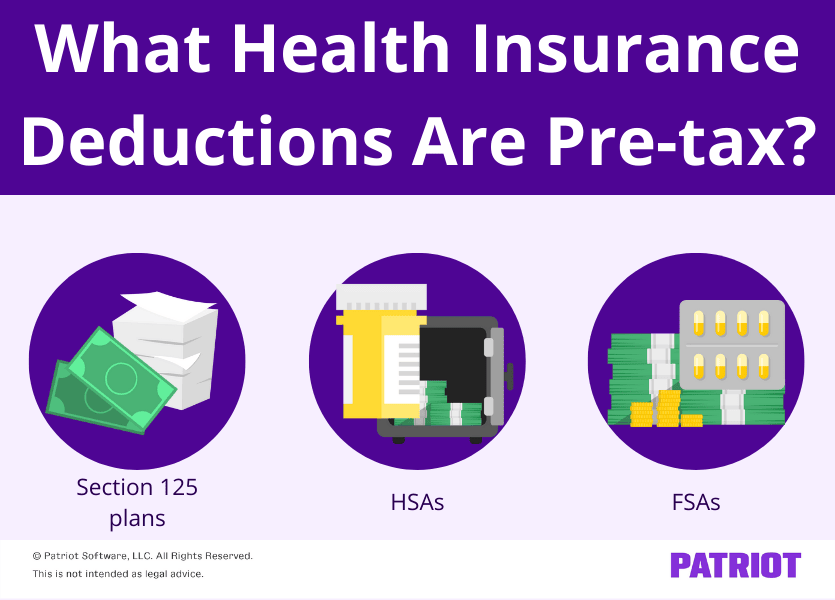

Pre-tax health insurance plans include:

- Section 125 cafeteria plans

- Health savings accounts (HSA)

- Flexible savings accounts (FSA)

Plans like health reimbursement arrangements (HRAs) offer similar pre-tax benefits (and we’ll get to that later).

Section 125 cafeteria plans

One of the most common types of medical insurance plans for employers is a Section 125 cafeteria plan. According to the IRS, Section 125 plans are written plans maintained by employers where all participants are employees, and participants can choose between two or more benefits. The benefits consist of cash and qualified benefits, and they’re not included in gross income. Typically, you cannot include benefits that defer an employee’s pay in the cafeteria plan.

Section 125 plans include qualifying benefits such as:

- Adoption assistance

- Dependent care assistance

- Accident and health benefits (not including Archer medical savings accounts)

- Group-term life insurance coverage

- Health savings accounts (HSAs)

Health savings accounts

What is an HSA? An HSA is a type of savings account specifically designed to help pay for or reimburse for certain medical expenses. Employees and self-employed individuals can only have an HSA if they have a high deductible health plan (HDHP).

HDHPs are health plans with high annual deductibles and low monthly premiums. You may have an HDHP Section 125 plan that pairs with a health savings account.

Health savings accounts are tax-free funds that the employee owns. Employers can contribute to the HSAs of their employees, but the employee has total ownership. If you contribute to an employee’s HSA and the employee does not, the employee still owns the funds. And, an employee can leave your company and take their HSA funds with them.

For 2026, individuals can contribute up to $4,400 each year for self-only coverage and $8,750 per year for family coverage. Employees can roll over funds to the following year, and the rollover funds do not count toward that year’s maximum contribution. Deduct the employee contributions before withholding taxes.

Flexible savings accounts

While similar to an HSA regarding taxability, a flexible spending account differs in a few critical ways:

- Only employees can open FSAs. Self-employed individuals cannot have a flexible savings account

- Employees can open an FSA regardless of the type of health insurance plan they have

- The employer owns the FSA account, not the employee. If an employee leaves, they forfeit their remaining FSA funds to the employer

- Employees receive their full funds at the start of the year. If they leave mid-year and spend more than they’ve contributed, they must pay the employer the difference

The maximum contribution for 2026 is $3,400. Employers can allow employees to roll over up to $680 in unused funds to the next year.

Deduct employee FSA contributions before withholding taxes.

How to calculate pre-tax health insurance

Employer-sponsored plans are typically pre-tax deductions for employees. In most cases, deduct the employee-paid portion of the insurance premiums before withholding any taxes.

However, pre-tax health insurance premiums may not come out before you withhold or contribute certain taxes. In some states, a pre-tax health premium is not pre-tax for certain taxes, such as state unemployment tax (e.g., Pennsylvania).

Let’s say you purchase a Section 125 cafeteria plan for your employees. The premiums are $600, and you pay 50% of the premiums. So, you deduct $300 from your employees’ paychecks and contribute $300 to the premiums.

You have an employee who earns $2,000 biweekly. Here is what the 7.65% FICA tax looks like with gross pay of $2,000 and no deductions:

$2,000 X 7.65% = $153

But, a Section 125 plan is pre-tax. So before withholding any taxes, deduct $300 for the pre-tax health insurance.

$2,000 – $300 = $1,700

After deducting the health insurance premiums, the employee’s pay is $1,700. Withhold the taxes for the employee based on $1,700 instead of $2,000. Take a look at the FICA tax now:

$1,7000 X 7.65% = $130.05

The employer portion of the FICA tax is lower, too, with pre-tax deductions. So, a pre-tax plan can also save you tax dollars by decreasing your tax liability.

Pre-tax vs. post-tax health insurance

Again, most employer-sponsored health insurance is paid for using pre-tax gross income. However, employees can still have post-tax premium payments. Employees who purchase coverage through an insurance company and do not elect to enroll in employer-sponsored plans have post-tax premiums.

The distinction between pre-tax or after-tax health insurance matters. Why? Because it determines how much your employees pay in taxes and their eligibility for other employer-sponsored benefits, such as HRAs.

Health reimbursement arrangements

Again, a health reimbursement arrangement allows employees to have pre-tax benefits even as they pay for their premiums with post-tax dollars. How? An employer can reimburse employees for medical costs, including payments on premiums, using nontaxable funds.

With HRAs, employees can choose the health plan they want or need. Take a look at three HRA options available to employers.

Qualified Small Employer Health Reimbursement Arrangement

A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is available for small employers who are not required to purchase company health insurance under the Affordable Care Act (ACA). A small employer under the ACA is one with fewer than 50 full-time equivalent (FTE) employees.

With a QSEHRA, employers can reimburse up to $6,450 for single employees or $13,100 for family coverage in 2026. Only small employers can set up and take advantage of a QSEHRA standalone plan. You can reimburse employees for individually-obtained premiums and any qualifying medical expenses (e.g., medication).

Individual Coverage Health Reimbursement Arrangement

Individual Coverage Health Reimbursement Arrangements (ICHRAs) are plans that allow employers to reimburse employees without contribution limits. Any employer can set up an ICHRA, but all applicable large employers (ALEs) as defined by the ACA must ensure the plan is affordable. ALEs are employers with 50 or more FTEs.

What does the ACA consider to be an affordable plan? The monthly premium for the lowest-cost Silver Health Plan for self coverage in the employee’s area (minus the monthly ICHRA reimbursement amount) must be less than 9.83% of one-twelfth of the employee’s household income.

Like a QSEHRA, an ICHRA is a standalone plan, so you cannot offer an ICHRA and an employer-sponsored traditional health insurance plan.

Excepted Benefit Health Reimbursement Arrangement

The third type of HRA is the Excepted Benefit Health Reimbursement Arrangement (EBHRA). The employer contribution to an EBHRA for 2026 is $2,200. Any employer, regardless of size, can create an EBHRA.

Unlike QSEHRAs and ICHRAs, you must also have a traditional health insurance plan in place. You cannot offer an EBHRA instead of traditional health insurance.

Reimbursements under EBHRAs cover any premiums not included in your traditional group plan (e.g., dental insurance), copays, and deductibles. You cannot use an EBHRA to reimburse your employees for premiums for the company health insurance plan.

Need a simple solution to deducting pre-tax insurance premiums from your employee’s paychecks? Patriot’s online payroll software automatically calculates every deduction and contribution you enter for accurate withholdings every time. Start your free trial today.

This article has been updated from its original publication date of June 21, 2021.

This is not intended as legal advice; for more information, please click here.