If you’re looking for a new benefit to offer employees, you might consider employer student loan repayment. The benefit itself isn’t new, but it got a tax-exemption makeover in 2020 thanks to the CARES Act and Consolidated Appropriations Act.

The result? An increasingly popular employee benefit hitting businesses nationwide. Here’s what you need to know about the employer student loan repayment program.

Employer student loan repayment: Background

When it comes to college, the United States breaks records … in student debt, that is. There’s a $1.6 trillion student debt balance.

Thanks to the student loan payment pauses since the pandemic, student debt has become an especially hot topic…

So, the government made it easier for employers to provide their employees with tax-free student loan repayment benefits. If you haven’t heard about the CARES Act employer-paid student loans, you’re not alone. It wasn’t the most promoted measure of taxpayer relief, after all.

Want to better attract talent? Or, do you want to offer student loan repayments in lieu of employee raises? Whatever your reason, read on to get your questions about loan repayment assistance programs answered.

What is employer student loan repayment?

Student loan assistance from employer is an employee benefit where the employer makes payments to pay for part or all of an employee’s student loans. Employers can either make payments (principal or interest) to the employee or the student loan lender directly.

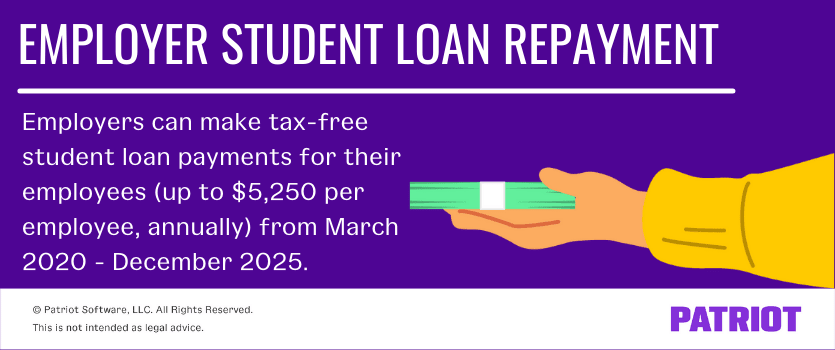

Prior to March 2020, student loan repayments of any amount were taxable. That all changed when the government passed the CARES Act and Consolidated Appropriations Act of 2020, making employer student loan repayments tax-free through December 2025.

The bottom line: Employers can make tax-free student loan payments (up to the IRS limit) until December 31, 2025, unless future legislation extends the deadline.

Want more articles like this?

Get the latest payroll news delivered straight to your inbox.

Subscribe to Email ListStudent loan repayment vs. educational assistance

Education assistance falls under Section 127 of the Internal Revenue Code. Whereas the student loan repayment is a new tax-free benefit, education assistance has been around for a while.

Employers can provide educational assistance to employees for current school-related costs an employee incurs, such as:

- Tuition

- Fees

- Books

- Supplies

- Equipment

So, what’s the difference between a student loan repayment program and an education assistance program? Turns out, there really isn’t a difference. The government simply expanded qualifying education assistance expenses to include student loan repayments.

The bottom line: Student loan repayments count as a qualifying educational assistance expense through the end of 2025.

What is the tax-free limit?

You can give each employee up to $5,250 per year toward student loan payments. Do not include this amount in the employee’s income.

Keep in mind that the tax-free amount of $5,250 is the combined limit for loan repayment and other types of education assistance under Section 127 of the Internal Revenue Code.

Include any amount you give an employee over $5,250 in the employee’s income (e.g., on Form W-2). Amounts over the tax-free limit are subject to taxes.

The bottom line: Is employer student loan repayment taxable? No, it is tax-free up to $5,250 per employee.

How popular is it?

In 2019, only 8% of companies offered this employee benefit. But because student loan repayment is now a tax-free benefit from 2020 – 2025 (and possibly beyond), that number has been increasing.

At the end of 2023, 34% of employers said they offered it, up from the 17% of companies that offered it in 2021.

Aetna, Estee Lauder, Fidelity Investments, and Staples are just a few companies that pay student loans for their employees.

The bottom line: Now that employer participation in repayment act is tax-free, more companies have started offering the benefit.

What loans qualify?

An employee’s loan qualifies for repayment if they took out a loan to pay qualifying education expenses that were:

- For themselves, their spouse, or a dependent

- Paid or incurred within a reasonable period of time (e.g., academic period) before or after taking out the loan AND

- For education provided during an academic period for an eligible student (aka someone enrolled at least half-time in a program leading to a degree, certificate, or other recognized educational credential)

You cannot give employees tax-free student loan repayments for loans they took out from a relative or qualified employer plan.

For more information, see IRS Publication 970.

The bottom line: Only qualifying student loans are eligible for tax-free status.

Should you consider paying your employees’ student loans?

An employer paying student loans may seem like a random benefit. After all, you don’t directly make payments for your employees’ other liabilities, like their mortgage or car loan. But unlike your employees’ other liabilities, student loan repayment is a tax-free employer benefit.

One in eight people in the United States has student loan debt. Due to large loans and high interest rates, student debt can make it difficult for employees to pay their other liabilities.

And if you can’t afford to give employees raises, adding tax-free benefits like student loan repayment might be the way to go.

You might consider implementing an employer student loan repayment program to:

- Retain employees

- Boost employee engagement and productivity

- Attract top talent

- Increase employee satisfaction and loyalty

And because student loan payments are tax-free through 2025, you don’t have to worry about paying employer Social Security or Medicare taxes on amounts up to $5,250.

The bottom line: Offering to help your employees pay their student loan bills is a tax-free way to boost your employer benefits.

What do you need to do to establish a program?

The IRS sets rules on what qualifies as an educational assistance program for tax purposes. To establish a qualifying student loan repayment program, you must:

- Have a written plan in place outlining the terms and conditions

- Not give more than 5% of total annual benefits to employees who own more than 5% of the company’s stock

- Not give employees a choice between educational assistance benefits and other taxable compensation

- Give reasonable notice of the program to eligible employees

- Not favor highly compensated employees

Consider including your student loan repayment plan information in your employee handbook.

The bottom line: Follow IRS guidelines on establishing educational assistance programs if you want your program to qualify.

This article has been updated from its original publication date of October 6, 2021.

This is not intended as legal advice; for more information, please click here.