Picture your star employees and how much value they add to your business. Many employers recognize their employees’ value with bonus pay. When you give an employee a bonus, you are required to withhold taxes on the additional money. To figure out how much to withhold, you need to understand the bonus tax rate.

Supplemental wages

Supplemental wages are additional dollars you give employees on top of regular wages. The following are considered supplemental wages:

- Bonuses

- Commissions

- Overtime pay

- Payments for accumulated sick leave

- Severance pay

- Awards

- Prizes

- Back pay

- Retro pay increases

- Payments for nondeductible moving expenses

As you can see, bonuses are supplemental wages. You must withhold the same taxes on supplemental wages that you withhold on regular wages. But, how you withhold them is different for supplemental pay.

Read on to learn the types of taxes you must deduct from employee pay and how to calculate tax on bonus pay.

Employment taxes

When you have employees, you don’t give them their gross wages. Gross pay is the total amount an employee earns before you take out payroll deductions.

Payroll deductions include taxes and benefits employees elect to receive. These are the taxes you are required to withhold from each employee’s wages:

- Federal income tax

- Social Security and Medicare taxes (FICA)

- State and local income tax (if applicable)

Federal income tax is based on an employee’s Form W-4, Employee’s Withholding Certificate. Your employee fills out Form W-4 when they are first hired. On Form W-4, employees can claim dependents or make withholding adjustments.

Use Form W-4 information with the tax withholding tables in IRS Publication 15 to determine the amount of federal income tax to withhold.

FICA tax is a flat rate of 7.65% that you withhold from each employee’s wages. Of this 7.65%, 6.2% goes toward Social Security tax and 1.45% goes toward Medicare tax. You also contribute a matching 7.65%.

There is a Social Security wage base limit, which is $176,100 in 2025. Only withhold and contribute 6.2% of the employee’s wages until the employee earns above the wage base.

There is no wage base limit for Medicare tax, but there is an additional Medicare tax. After an employee earns $200,000, withhold 0.9% in addition to 1.45% for Medicare. But, you do not contribute to additional Medicare tax.

State and local income tax liabilities depend on where your business is located. If there is state and local income tax in your business’s locality, withhold the appropriate amount.

Employment taxes come out of an employee’s bonus pay. You must withhold federal, state, and local income tax as well as FICA tax from each employee’s supplemental wages. And, supplemental wages can affect the amount you pay for FUTA tax.

Bonus tax rate

Here are a few frequently asked questions about bonus pay tax:

- Are bonuses taxed at a higher rate than regular wages?

- How much are bonuses taxed?

- How are bonuses taxed?

Taxes on bonuses follow the rules for federal income tax on supplemental wages. They can be taxed one of two ways:

- Percentage method

- Aggregate method

There is also a separate bonus tax rate for employees who receive more than $1 million in supplemental wages in one calendar year.

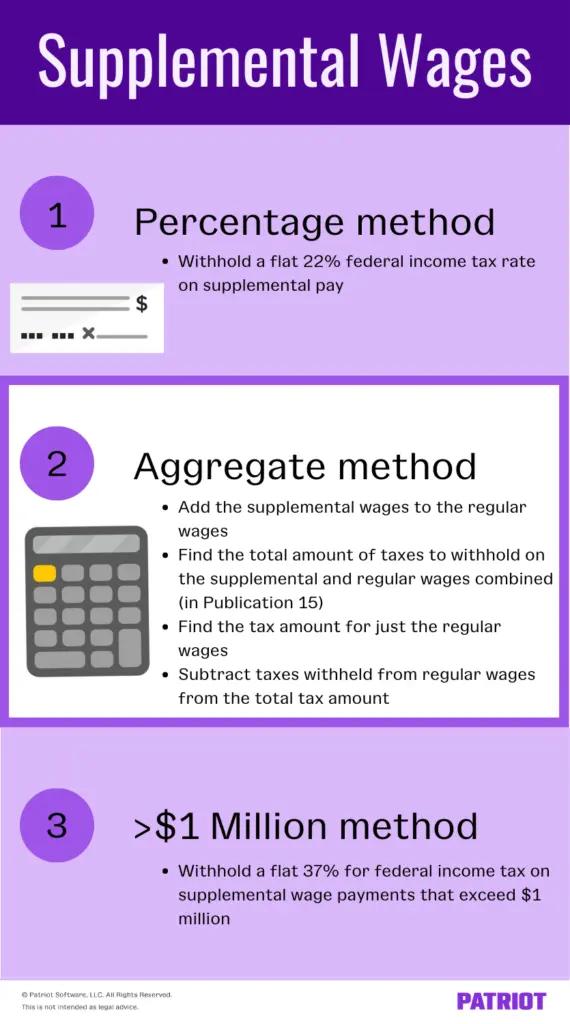

1. Percentage method

The percentage method is easier than the aggregate method, making it popular among small business owners. Withhold a flat 22% federal income tax rate on bonus pay with the percentage method.

You will withhold taxes on the employee’s regular wages like normal. The tax on bonus payments is separate from regular wages.

Percentage method example

Let’s say you have a single employee with two allowances claimed on Form W-4. They earn $500 each week. One week, the employee receives a bonus of $400. To find how much federal income tax to withhold, separate regular and bonus wages.

- First, find out how much to withhold from the $500 (regular wages). Use the wage bracket method in Publication 15 to determine tax withholding on the employee’s regular wages.

- Next, find out how much to withhold from the $400 (bonus pay) using the percentage method. Multiply $400 by 22% ($400 X 0.22). Withhold $88 from the bonus pay.

In addition to the employee’s regular income tax withholding, you must withhold $88 from the employee’s bonus pay.

2. Aggregate method

The aggregate method is a little more complex than the percentage method. For the aggregate method, you will add the bonus wages to the regular wages that are paid at the same time.

Here’s a step-by-step process:

- Add the bonus wages to the regular wages.

- Use the total wages (bonus wages + regular wages) and Publication 15 to find the total amount to withhold.

- Find the tax amount in Publication 15 for just the regular wages.

- Subtract the taxes withheld from the regular wages from the total tax amount to determine the bonus tax amount.

- The remaining number is the bonus tax rate, so you will withhold that from the bonus pay.

If your employee is worried that the method you use takes more out of their wages, remind them that they might receive a refund to even out the withholdings during tax season.

- Multiple pay rates

- Repeating money types

- All pay frequencies

>$1 million method

If an employee earns more than $1 million in supplemental wages (not including regular wages) in one calendar year, you need to follow special rules. Withhold 37% for federal income tax on supplemental wage payments that exceed $1 million.

This 37% usually applies to large corporations whose employees receive high commissions and bonuses.

For example, an employee earns $1,200,000 in supplemental wages. Since they earn $200,000 over the $1 million threshold, you must withhold 37% on the excess. To figure out how much money to withhold on the excess, multiply $200,000 by 37%. Withhold $74,000 ($200,000 X .37).

Other taxes

You will also be required to withhold FICA tax from your employees’ bonus wages. The FICA tax rate is still the standard 7.65% on bonus pay. Don’t forget to take into account the Social Security wage base limit and the additional Medicare tax.

If there are state and local income taxes in your locality, you will also need to withhold those from the employee’s bonus wages.

Need an easy way to track bonus payments? Patriot’s online payroll software lets you enter bonus payments when you run payroll. That way, you know how much you pay employees in regular wages as well as supplemental wages. Get your free trial today!

This article has been updated from its original publication date of September 1, 2017.

This is not intended as legal advice; for more information, please click here.