Here’s the scoop: 72% of private industry workers have access to employer-provided retirement plans. Do yours? If you don’t offer employees a small business retirement plan, like a 401(k), it might be time to hop on the bandwagon. Read on to learn about the types of 401(k) plans to choose from.

About 401(k) plans

A 401(k) plan is an employer-sponsored retirement plan offered as an employee benefit. Employees can choose how much they contribute each paycheck to their retirement plan, and there are several retirement plan features that simplify contributions. When the employee reaches a certain age or meets certain criteria, they can make withdrawals.

The types of 401(k) options come with tax benefits to the account holder. Some 401(k) plan contributions are pre-tax while others are post-tax.

Employers can contribute to employee 401(k) plans, too. In fact, some plans require employer contributions.

If you contribute to a 401(k) plan as an employer, set rules for contributions, such as a waiting period (e.g., employees must work for you for six months before you begin contributing). Also, you may limit the amount you contribute (e.g., you match 50% of the employee’s contribution, up to 8%).

Limit alert! The IRS limits the amount an employee or employer can contribute to a 401(k) plan. This limit can change annually.

Why should you offer a 401(k) plan?

On the fence about including a 401(k) plan in your employee benefits package? Here are a few reasons to offer a 401(k) plan:

- Employee attraction and retention: 81% of employees said retirement benefits are important during a job search

- Tax credits: You may be eligible to claim 401(k) tax credits (with enhanced tax credits thanks to the SECURE Act)

- State requirements: Some states require employers to provide retirement plans to employees (e.g., California)

Improving your employer brand and scoring tax credits are two added bonuses for voluntarily beefing up your benefits package with a retirement plan. But if you’re subject to a state-mandated retirement plan, the choice isn’t yours—you must provide a retirement option to stay compliant.

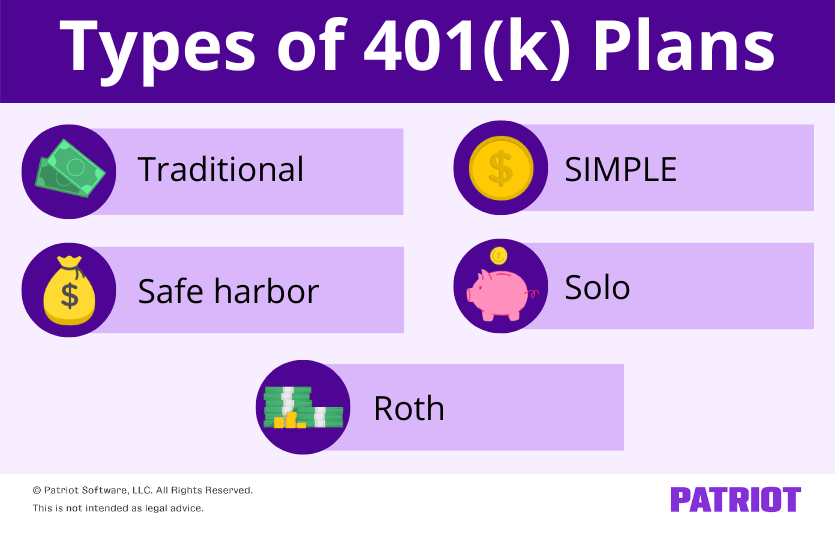

Types of 401(k) plans

So, what options do you have when it comes to 401(k) plans? Here are the different types of 401(k) plans you can have at your business:

- Traditional 401(k) plans

- Safe harbor 401(k) plans

- SIMPLE 401(k) plans

- Roth 401(k) plans

- Solo 401(k) plans* (not for employees)

Most retirement plans can be combined with other plans. For example, employees can have both traditional and Roth 401(k) plans.

401(k) types can vary in terms of flexibility, 401(k) contribution limits, and plan requirements. Compare each 401(k) plan option before making a decision on which route to go for your company.

Traditional 401(k) plans

Under a traditional plan, employees contribute a portion of their wages before income taxes to their 401(k). However, withhold Social Security and Medicare (aka FICA tax) taxes on the employee’s gross pay before deducting the employee’s 401(k) contribution.

With this plan, some employers match a portion of the employee’s 401(k) contributions (e.g., 50% up to 6%). Employer matching and nonelective contributions are not subject to FICA or federal income tax.

Traditional 401(k) plan requirements

Who can offer a traditional plan: A private or public employer of any size can offer a traditional plan to employees.

Contribution requirements: You can either contribute for all participants (even if they don’t contribute), make matching contributions based on an employee’s elective deferral, or both. You can subject contributions to a vesting schedule where your employer contributions to an employee’s plan become nonforfeitable after a certain amount of time (e.g., three years).

Contribution limit: Employees can defer up to $23,500 to their 401(k) retirement plan in 2025. Employees who are 50 or older can contribute an additional catch-up contribution that can also change annually. The additional contribution limit for 2025 is $7,500. There’s a special catch-up contribution of $11,250 for employees aged 60, 61, 62, or 63 in 2025. The amount of employer and employee contributions combined cannot be larger than the annual limit. The limit must be the lesser of 100% of the employee’s compensation or $70,000 for 2025.

Plan requirements: To set up a traditional 401(k) plan, create a plan document that follows IRS rules, establish a trust for the plan’s assets, maintain good 401(k) records (e.g., contributions and values), and provide information to participating employees.

Filing requirements: File Form 5500, Annual Returns/Reports of Employee Benefit Plan each year to report employee benefit plan information.

If you choose a traditional 401(k) plan, you must conduct an annual nondiscrimination test to ensure the contributions don’t just benefit highly compensated employees. The test compares the average salary deferrals of highly compensated employees to non-highly compensated employees. Perform and pass the Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) tests to keep a traditional 401(k) plan. Check the IRS’s website for more information on the ADP and ACP tests.

Safe harbor 401(k) plans

A safe harbor 401(k) plan is a special type of retirement plan that automatically passes the nondiscrimination test. This means that you don’t have to pass an ADP and ACP test each year as you do with a traditional 401(k) plan.

Safe harbor 401(k) plans are popular with small businesses because employers can avoid the time and money it takes to pass nondiscrimination tests each year. But there’s one caveat: you are required to contribute to an employee’s safe harbor retirement plan.

With a safe harbor plan, you must contribute to an employee’s 401(k), regardless of their title, compensation, or length of service.

Safe harbor 401(k) plan requirements

Who can offer a safe harbor plan: Businesses of any size can offer a safe harbor 401(k) plan.

Contribution requirements: You must make either an eligible matching (basic or enhanced) or nonelective contribution. A basic match is a 100% match on the first 3% of deferred compensation, plus an additional 50% for each contribution that is over 3% but under 5%. An enhanced match is a 100% match on the first 4% of deferred compensation. A nonelective contribution is 3% (or more) of compensation, regardless of employee deferrals. Employer contributions are required to be fully vested, and your employees are guaranteed your contributions to their safe harbor 401(k) plan.

Contribution limit: The contribution limit for a safe harbor 401(k) plan is the same as a traditional 401(k) plan. Employees can defer up to $23,500 (2025) and the additional contribution limit for 2025 is $7,500 (or $11,250 for those ages 60, 61, 62, and 63). The amount of employer and employee contributions combined cannot be larger than the annual limit. The limit must be the lesser of 100% of the employee’s compensation or $70,000 for 2025.

Plan requirements: Employers must give each eligible employee a written notice that lists their rights and obligations. Provide written notice to eligible employees before each plan year.

Filing requirements: Like traditional 401(k) plans, file Form 5500 each year if you have a safe harbor plan.

SIMPLE 401(k) plans

A SIMPLE 401(k) plan is ideal for small business owners or self-employed professionals with 100 or fewer employees. This type of plan is a simplified version of a traditional 401(k) plan.

A SIMPLE 401(k) plan combines the features of a traditional plan with the simplicity of a SIMPLE IRA. And with a SIMPLE 401(k), you don’t need to perform nondiscrimination tests.

Under a SIMPLE 401(k) plan, your contributions are nonforfeitable as soon as you contribute them. However, employees who participate in a SIMPLE 401(k) plan cannot receive contributions and accruals with any other employer-sponsored retirement plan.

Simple 401(k) plan requirements

Who can offer a SIMPLE 401(k) plan: Small businesses with 100 or fewer employees can offer a simple 401(k). If your business exceeds the 100-employee limit, there’s a two-year grace period before you need to change your 401(k) plan. To qualify for the grace period, you must have had a SIMPLE 401(k) plan for at least one year and no longer qualify due to business growth.

Contribution requirements: You must contribute to your employees’ plans. Both the employee and employer contributions are pre-tax. As an employer, you must make either a matching contribution of up to 3% of each employee’s pay or a nonelective contribution of 2% of each eligible employee’s pay.

Contribution limit: Employees can only contribute up to $16,500 in 2025 under a SIMPLE 401(k) plan. Employees who are 50 years or older can contribute up to an additional $3,500 for 2025. Employees who are ages 60, 61, 62, and 63 can contribute up to an additional $5,250 for 2025.

Plan requirements: To establish a SIMPLE 401(k) plan, create a written plan, get it approved by the IRS, and explain the written plan to your employees.

Filing requirements: File Form 5500 if you have a SIMPLE 401(k) plan at your business.

Roth 401(k) plans

A Roth 401(k) plan has similarities to a traditional 401(k). But with a Roth 401(k), you deal with post-tax deductions instead of pre-tax. Withhold taxes from an employee’s gross pay before you defer their wages to the 401(k) plan.

When an employee retires, withdrawals from traditional 401(k) accounts are taxed at ordinary income rates. But with a Roth 401(k), withdrawals are generally tax-free.

Like the traditional 401(k) plan, you also need to perform annual nondiscrimination testing on Roth 401(k) plans. A Roth 401(k) plan must be a separate account from the other 401(k) plans you offer. Here’s everything you need to know about establishing a Roth 401(k) plan for your employees.

Roth 401(k) plan requirements

Who can offer a Roth 401(k) plan: Businesses of any size can offer a Roth 401(k) plan.

Contribution requirements: Employers are not required to contribute to employees’ Roth 401(k) plans. However, you can choose to match your employees’ contributions to a Roth 401(k) plan.

Contribution limit: Employees can contribute a maximum of $23,500 to their Roth 401(k) plan in 2025. Employees age 50 or older can contribute an additional $7,500 in 2025 ($11,250 for those ages 60, 61, 62, and 63).

Plan requirements: You must offer a traditional 401(k) plan in addition to a Roth plan. Create a plan document, establish a trust for the plan’s assets, and provide information to participating employees.

Filing requirements: File Form 5500 annually.

Solo 401(k) plans*

You cannot offer a solo 401(k) plan to your employees. A solo 401(k) plan only has one participant—you. It’s a traditional 401(k) plan designed specifically for a business owner or self-employed individual with no employees apart from their spouse or business partners. This type of plan is also called an individual 401(k), self-employed 401(k), or solo-k.

The plan allows the employer to make contributions as both an employer and an employee. This allows business owners to maximize retirement contributions and business deductions. All contributions you make are tax-deductible.

Solo 401(k) plan requirements

Who can offer a solo 401(k) plan: Sole proprietors, self-employed individuals, small business owners, or individuals with no employees except for a spouse or partners.

Contribution requirements: You can contribute as both the employee and the employer. You do not have to contribute as the “employer.”

Contribution limit: In a solo 401(k), you’re both the employee and the employer. As the employee, you can contribute up to $23,500 or 100% of compensation (whichever is less) for 2025 AND make an additional profit-sharing contribution of up to 25% of your compensation. If you are over 50 years old, an additional $7,500 catch-up contribution ($11,250 for those ages 60, 61, 62, and 63) is allowed for 2025. Your total contribution (excluding catch-up contributions) cannot exceed $70,000 in 2025.

Plan requirements: If you have an Employer Identification Number (EIN), you can open a solo 401(k) account as long as you meet eligibility requirements.

Filing requirements: File Form 5500-EZ, Annual Return of One-Participant (Owners and Their Spouses) Retirement Plan annually.

401(k) types: Quick-reference chart

For all you skimmers out there, here’s a quick comparison chart of the different types of 401(k). Use it to compare requirements, contribution limits, and employer contribution requirements.

| 401(k) Type | Who Can Establish the Plan? | Contribution Limit (2025) | Do Employers Need to Contribute? |

|---|---|---|---|

| Traditional 401(k) Plan | Anyone | Employees under 50: $23,500 Catch-up contribution for employees aged 50 and up: $7,500 Catch-up contribution for employees aged 60, 61, 62, and 63: $11,250 | No |

| Safe Harbor 401(k) Plan | Anyone | Employees under 50: $23,500 Catch-up contribution for employees aged 50 and up: $7,500 Catch-up contribution for employees aged 60, 61, 62, and 63: $11,250 | Yes |

| SIMPLE 401(k) Plan | Employers with 100 or fewer employees | Employees under 50: $16,500 Catch-up contribution for employees aged 50 and up: $3,500 Catch-up contribution for employees aged 60, 61, 62, and 63: $5,250 | Yes |

| Roth 401(k) Plan | Anyone | Employees under 50: $23,500 Catch-up contribution for employees aged 50 and up: $7,500 Catch-up contribution for employees aged 60, 61, 62, and 63: $11,250 | No |

| Solo 401(k) Plan | Businesses with NO employees (except for a spouse or partners) | Employees under 50: $23,500 Catch-up contribution for employees aged 50 and up: $7,500 Catch-up contribution for employees aged 60, 61, 62, and 63: $11,250 | N/A |

Other types of retirement plans

Again, the different 401(k) plans aren’t the only retirement options you can offer employees. You might be able to offer the following types of retirement plans:

- Individual Retirement Arrangement (IRA)

- Roth IRA

- 403(b) plan

- SIMPLE IRA plan

- Simplified Employee Pension (SEP) plan

- Salary Reduction Simplified Employee Pension (SARSEP) plan

- Profit-sharing plan (PSP)

- Employee stock ownership plan (ESOP)

To learn more about your retirement plan options for your business, head on over to the IRS’s website.

This article has been updated from its original publication date of May 21, 2012.

This is not intended as legal advice; for more information, please click here.