You may have an employee whose wages are subject to garnishment at some point. What is a wage garnishment? And what do you need to do?

Jump Ahead

- What is a wage garnishment?

- Garnishment laws

- Who’s involved in wage garnishment?

- Employer wage garnishment guidelines

- What does a garnishment look like on a pay stub?

What is a wage garnishment?

Garnishment is a method of collecting money from a person with overdue debts. When an employee has unpaid debts, a court or government agency might order you to withhold extra money from their paycheck. The withheld wages go toward repaying the employee’s debts.

Most garnishments are court-ordered. The IRS, state tax collection agencies, and other non-tax government agencies can also order garnishments for unpaid debts.

Types of debts that lead to garnishment

A creditor may seek a garnishment to collect unpaid debts such as:

- Overdue child support

- Unpaid taxes

- Defaulted government student loans

- Delinquent credit card loans

- Outstanding medical bills

Garnishment laws

Both federal and state laws that protect employees who are subject to wage garnishment. Understand garnishment laws to avoid penalties and jail time.

Federal garnishment law

Federal wage garnishment law protects employees by placing restrictions on the garnishment process under Title III of the Consumer Credit Protection Act. Employers who violate Title III may face a fine, jail time, or both.

The Consumer Credit Protection Act:

- Limits the amount that can be garnished

- Provides job protection to employees with a garnishment for one debt

State garnishment laws

Some states have laws about garnishing employee wages. For example, the state might set lower garnishment limits or protect employees with more than one garnishment.

If your state has garnishment laws that are more favorable to your employee, follow state laws. Otherwise, follow the federal regulations. Look up garnishment laws by state for more information.

Who’s involved in wage garnishment?

There are several parties involved in wage garnishments, including:

- Creditors: A creditor can involve the courts to satisfy a debt, such as child support, through garnishment.

- The courts: The courts issue a garnishment order that involves a third-party (e.g., employer) and requires them to pay some or all of the debt.

- Government agencies: Sometimes, government agencies get involved in and order garnishments. For example, the IRS may issue a wage garnishment if an employee owes taxes.

- Employers: The employer, or “garnishee,” is responsible for complying with a wage garnishment order by withholding and remitting payments. Employers are also responsible for complying with wage garnishment laws.

- Employees: The employee is the party whose wages are subject to garnishment.

Employer wage garnishment guidelines

Dealing with payroll taxes and other deductions can be complicated if you run payroll by hand. Receiving a garnishment order can add to that stress, especially if you’ve never been a garnishee before.

Take a look at the following employee garnishment rules to get started.

1. How does a wage garnishment work?

If you need to garnish an employee’s wages, you will receive a garnishment order telling you so. Withhold the employee’s wages according to the order.

You might have to answer the order. If so, you must send proof that you employ the worker and report how much they earn. The sender might also require additional information.

If the garnishment order lists an end date, ensure you carefully read the order and end on the correct date—even if there’s remaining debt. Or, the agency that sent the order may send a “Notice of Termination of Wage Garnishment Order” that tells you when to stop the garnishment.

2. Which wages can be garnished?

Most types of wages are subject to garnishment. These include:

- Hourly wages

- Salaries

- Bonuses

- Commissions

- Pension or retirement plan income

Tip income is generally exempt from garnishments.

Only an employee’s disposable earnings are subject to garnishment. Disposable earnings are what is left after you subtract legally required deductions from an employee’s wages, such as federal, state, and local taxes. Do not subtract non-required deductions, such as health and life insurance and retirement plan contributions, when calculating disposable earnings. As a result, an employee’s disposable earnings and net pay might differ.

3. How much to withhold

The garnishment order will tell you how much to withhold from your employee’s wages. However, garnishment laws may protect some of the employee’s wages from garnishment to ensure that the employee has enough take-home pay. You might withhold less than the garnishment order states.

Follow the garnishment limits to avoid withholding too much from the employee’s wages. The order should include a calculation worksheet to ensure you withhold the correct amount.

The Consumer Credit Protection Act protects the garnishee by limiting the amount of wages that can be garnished. The maximum amount that can be garnished from wages depends on the type of debt.

Garnishments for judgment creditors

A judgment creditor is someone who wins a monetary award in a lawsuit.

If a judgment creditor garnishes wages, they cannot take more than:

- 25% of the employee’s disposable earnings, or

- The amount that the employee’s disposable earnings exceed 30 times the federal minimum wage, which is $7.25

Let’s say an employee earns $500 in disposable personal income per week. Twenty-five percent of the disposable income is $125. The amount that the disposable income exceeds 30 times the federal minimum wage ($7.25 X 30 = $217.50) is $282.50 ($500 – $217.50). You can only garnish up to the lower of the two numbers. This means the most you can garnish from the employee’s disposable income is $125.

U.S. Department of Labor Fact Sheet #30 has a chart to help determine the maximum amount you can garnish.

Child support and alimony

If the employee does not support another spouse or child, up to 60% of disposable personal income can be garnished for child support or alimony. If the employee does support another spouse or child, you can garnish up to 50% of disposable earnings for alimony or child support withholding. For payments that are more than 12 weeks overdue, an additional 5% can be added.

Non-tax federal debts

Agencies that fall under the Debt Collection Improvement Act can garnish up to 15% of disposable earnings for debts owed to the federal government.

Department of Education agencies can also garnish up to 15% of disposable earnings for defaulted federal student loans.

Non-tax federal debts are subject to federal garnishment laws for maximum wages garnished in a pay period. They are not subject to any state garnishment laws.

Exceptions to wage garnishment limits

Maximum garnishment restrictions typically do not apply to bankruptcy court orders or unpaid federal or state taxes. That means there is no garnishment cap for unpaid taxes and bankruptcy court orders.

4. Job protection

Under federal law, you cannot fire an employee because of a garnished debt. However, this federal protection applies if an employee’s pay is garnished for only one debt. According to the Department of Labor, “The CCPA does not prohibit discharge because an employee’s earnings are separately garnished for two or more debts.”

Your state may have further protections. Check with state garnishment laws for more information.

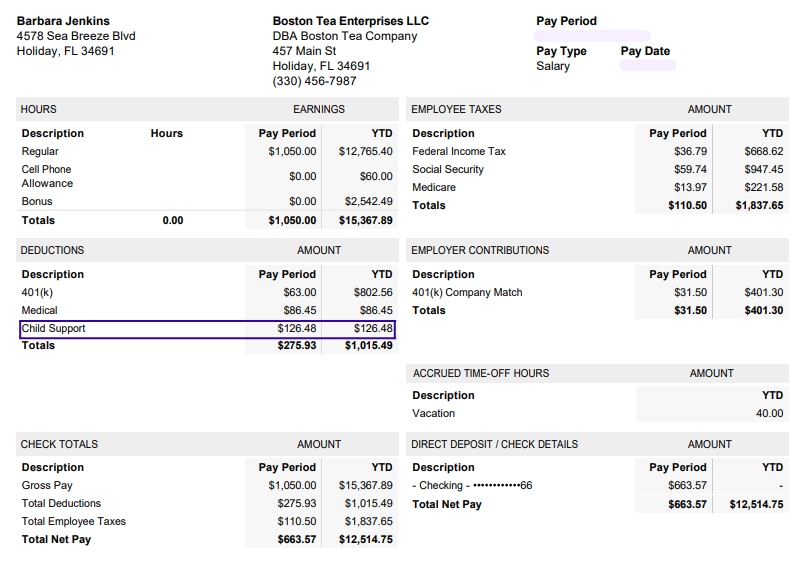

What does a garnishment look like on a pay stub?

You and your employee might wonder how a garnishment appears on a pay stub. Let’s say you receive a garnishment order for child support.

Here’s how the garnishment would look on a pay stub:

Whether an employee has a garnishment or not, payroll is confusing. Patriot Software’s online payroll makes it easier. You can set up deductions, such as garnishments, and we’ll do the calculations for you. Try it today!

This article is updated from its original publication date of February 29, 2016.

This is not intended as legal advice; for more information, please click here.