Looking to offer your employees an additional benefit? Consider creating a profit-sharing plan. But before you run off and create a plan, you need to know what is profit sharing. Read on to learn all about profit sharing, including how it works and steps for creating a plan of your own.

What is profit sharing?

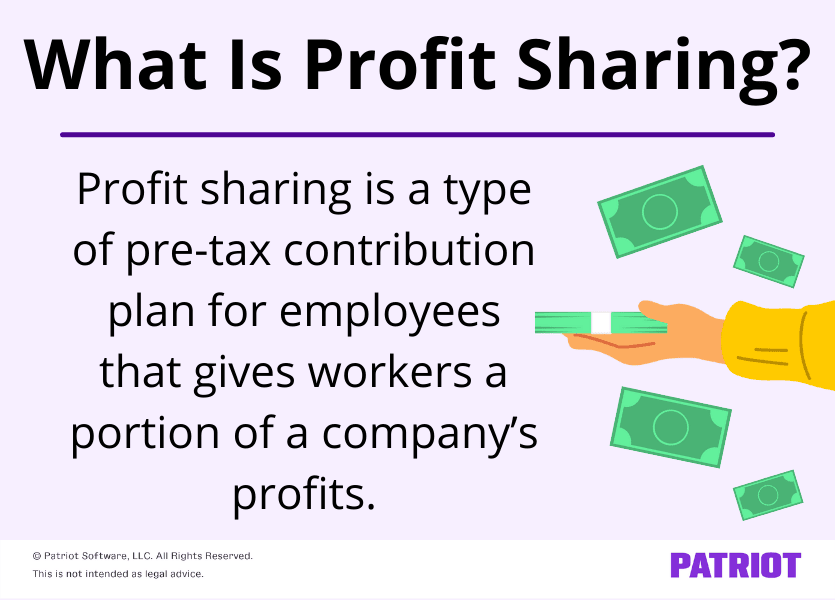

Profit sharing is a type of pre-tax contribution plan for employees that gives workers a certain amount of a company’s profits. The profit-sharing payments depend on the:

- Business’s profitability

- Employee’s regular wages and bonuses

- Amount set by the business

With a profit-sharing plan (PSP), employees receive an amount based on the company’s earnings over a specific period of time (e.g., a year). Generally, an employee receives a percentage or dollar amount of the business’s profits either in cash or company stock. Many businesses offer profit sharing as a retirement benefit for employees.

If an employer does not make a profit during the time period (e.g., year), they do not have to make contributions that year.

Typically, a business offers a PSP to help instill a sense of ownership in its employees. The goal of a small business profit-sharing plan is to reward employees for their contribution to the company’s success and incentivize employees to keep reaching goals.

PSP vs. 401(k)

Although a profit share agreement can be used as a retirement plan option to offer employees, it’s not the same as a 401(k) plan.

Both plans give employees additional retirement benefits. However, 401(k) plans and PSPs have different rules and structures.

With 401(k) plans, employees can make contributions to their own plans. And depending on the type of 401(k) plan, the employer might make a matching contribution.

With a PSP, an employee cannot make any contributions. Only the employer can make a contribution to the PSP. But, a company can offer other types of retirement plans, such as 401(k), along with a PSP.

Types of PSPs

There are a few different types of profit-sharing plans to choose from. They all follow the same concept: an employer sharing a portion of their profits with employees.

Here are the three types of PSPs:

- Pro-rata: All employees receive the same contribution amount from the employer (e.g., percentage or fixed dollar). This is the most common type of PSP.

- Non-comparability / cross-testing: Employers can contribute to different groups of employees (e.g., full-time employees) at different rates.

- Age-weighted: Takes age and salary into consideration. Employers can offer older employees a higher percentage than younger employees because they are closer to a retirement age. With an age-weighted plan, the longer someone stays with the business, the more their employer contribution rate increases. This type is specific to PSPs used as retirement plans.

Requirements for a PSP

Businesses of any size can create a profit-sharing plan. If you use your PSP as a retirement benefit, you can also take advantage of other retirement plan types.

A business must also follow a predetermined profit allocation formula for deciding how much employees receive in profits and which employees are eligible.

There’s no set amount that a company must contribute to its PSP each year. But, there is a maximum contribution amount that you can make per employee. According to the IRS, the contribution limit for a company sharing its profits with an employee is the lesser of 25% of that employee’s annual compensation or $69,000 (2024).

Profit sharing example

Ready to see profit sharing in action? Let’s look at an example of profit sharing so you can see it first-hand.

To calculate the employer contribution, you need to add the compensation for all employees. Divide each employee’s individual compensation for the period by the total compensation for the period. Then, multiply your profit share percentage by your profits for the period. Finally, multiply the two totals together to determine each employee’s payment amount.

Say you have three employees. Employee A makes $30,000 per year, Employee B makes $25,000, and Employee C makes $40,000. The total compensation for all three employees is $95,000 ($30,000 + $25,000 + $40,000). This year, your business had a profit of $150,000, and you share 10% of your annual profits with employees. Take a look at how much each employee would receive:

Employee A: ($150,000 X 0.10) X ($30,000 / $95,000) = $4,736.84

Employee B: ($150,000 X 0.10) X ($25,000 / $95,000) = $3,947.37

Employee C: ($150,000 X 0.10) X ($40,000 / $95,000) = $6,315.79

To figure out your company’s profit-sharing amount per employee, you can use the following formula:

Profit-sharing amount = (Profits X Profit-sharing Percentage) X (Employee Compensation / Total Employee Compensation)

How to create a profit-sharing plan

To get started creating your PSP, follow the steps below:

- Determine how much you want your PSP amount to be

- Profit allocation formula

- Percentage vs. dollar amount

- Write up a plan

- Rules

- Eligibility requirements

- Amount (e.g., percentage or dollar amount)

- Frequency (e.g., annual)

- Provide information to eligible employees

- File IRS Form 5500 annually

- Details your contribution plan and all participants in it

- Keep records (e.g., amounts, participants, etc.)

Benefits and disadvantages of profit sharing

There are pros and cons to profit sharing. Before you start small business profit sharing, weigh the advantages and disadvantages.

Here are some benefits of a profit-sharing plan for businesses:

- You can change how much you contribute year to year

- Any business can start one

- You can offer one in addition to other retirement plans

- Plans boost employees’ commitment to the business for the long-term

- It can be used to attract and retain top talent

- The plan can motivate your team

- Contributions are tax-deductible for employers

Check out some cons to a PSP:

- Takes some extra work to get set up (e.g., filling out Form 5500)

- Employer is subject to nondiscrimination testing

- Employees can’t contribute

- You may need to do some tweaking when calculating an employee’s pay

- The plan’s only focus is profitability

Do your research and determine if the cons are worth it before you decide to follow the path of profit sharing.

This article has been updated from its original publication date of July 12, 2013.

This is not intended as legal advice; for more information, please click here.